24/7 Emergency Claim

Blog of Carnaghan Thorne Insurance

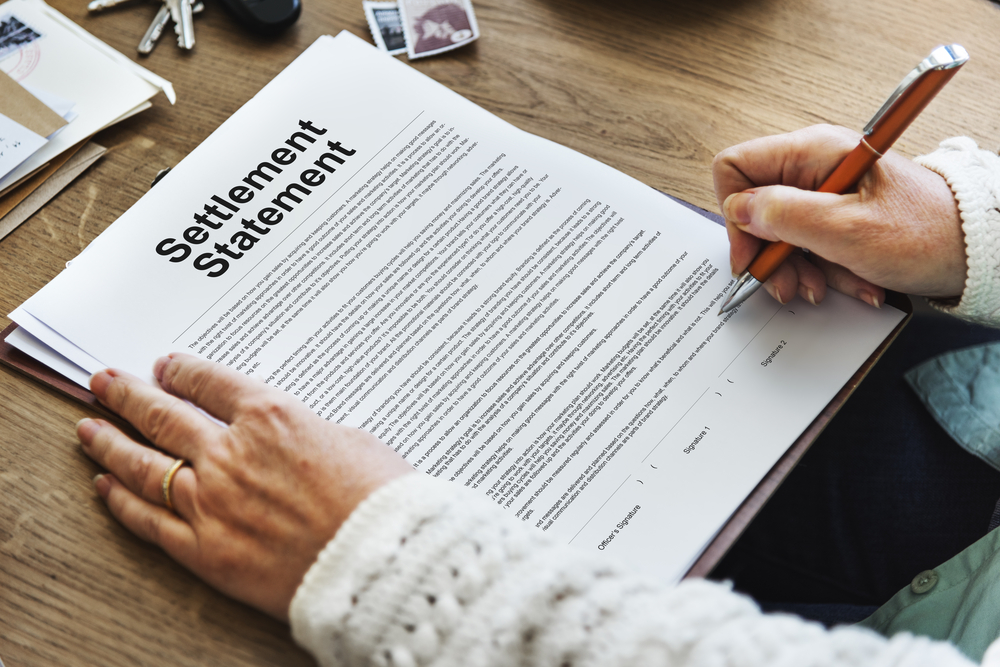

Settlements—Actual Cash Value vs. Replacement Cost

Insurance is an essential fact of life that most adults have encountered as they have purchased homes, vehicles, or rental properties. While having an excellent insurance broker is a good place to start, it’s also important to investigate your options.

The terms “Actual cash value” and “replacement cost” aren’t necessarily interchangeable on insurance documents. These numbers can be very different when the time comes to collect the insurance amount.

Protect Your Seasonal Home and Summer Toys

There is always something attractive and alluring about the warm, summer months, and the long, bright days. From backyard barbecues, to weekends at your lakeside cottage, and road trips in your RV, these months promise a ton of fun with family and friends. With a host of exciting, social engagements, and a variety of outdoor activities, who wouldn’t look forward to the warm season?

How the Internet of Things (IoT) is Changing the Way we Look at Home Insurance

These days, the Internet of Things (IoT) has touched almost everything in modern society and insurance rates are no exception. Fortunately, data analytics captured through connected IoT solutions are a benefit to both insurance companies and clients. The ability to harness the power of a wireless connection into almost any physical object has no doubt transformed the landscape of the insurance industry in recent years and will continue to do so in the years that follow. For example, in 2016, 80 million smart-home devices were delivered globally. With a projected growth rate of 60%, that means over 600 million of these appliances could be in use by the year 2021.

Comprehensive Auto Coverage

In New Brunswick, auto insurance is mandatory for all vehicle owners and a standard policy will protect you in a number of ways. However, many drivers feel that this coverage is inadequate to fully protect them. Comprehensive coverage can add the missing components to your insurance plan and result in supplying you the full protection you desire. In this blog entry, we’ve included helpful information on automobile insurance that Saint John motorists can put to good use. Read on to see how you can avoid many insurance-related headaches.

Protecting Your Property on Accommodation Apps

Our world has changed with technology making its way into our lives like never before, creating both challenges and opportunities. One of these technologies has seen growth of what has been called the “shared economy” and is allowing Canadians to rent their homes to travelers via online vacation rental services such as Airbnb, HomeAway, and VRBO.

New Brunswick’s Mandatory Auto Coverage

Carnaghan Thorne Insurance offers coverage plans for your house, business, personal property, construction site, and vehicle of any kind with access to multiple coverage options – including mandatory coverage. If you own and operate an automobile in New Brunswick, you are required by law to insure it. The mandatory coverage in New Brunswick is comprised of Third-Party Liability, Direct Compensation – Property Damage, Uninsured Automobile Coverage, and Accident Benefits.

In the case of Third-Party Liability, if you are responsible for an accident causing injuries or fatalities, or if your vehicle damages someone else’s property, you may be legally responsible. Minimum coverage for Third-Party Liability is $200,000, but most drivers choose $1 million.

Misconceptions about Car Insurance

There are many misconceptions floating around about car insurance, some of which may affect the type of car you purchase. Owning and operating a car can be expensive enough without wasting money because you don’t understand your auto insurance policy. Many Canadians are putting themselves, their families, and their assets at risk by making misinformed decisions about their insurance based on hearsay and insurance urban legends.